Another issue individuals contemplating divorce must resolve is who gets to claim the Dependency Exemptions for the children. In general, a taxpayer may claim a Dependency Exemption for each child who is under age 19, or under age 24 if a full-time student, and lived with the taxpayer for more than ½ of the year, except for temporary absences including time away at school. The child must not provide more than ½ of their own support, excluding scholarships received. In the case of divorced or legally separated parents the exemption will go to the parent who has primary custody as determined by the number of nights in the parent’s home. If the custodial time is equal for both parents, the exemption (and the title of custodial parent) goes to the parent with the higher adjusted gross income. The Dependency Exemption in these situations may be waived by the custodial parent and transferred to the non-custodial parent by signing a Form 8332 which the non-custodial parent must attach to their income tax return.

Note that the ability of the taxpayer to claim Head of Household filing status stays with the custodial parent whether or not they may have waived the Dependency Exemption. The child tax credit on the other hand may only be claimed by the parent that actually claims the Dependency Exemption.

The experts in our tax department have navigated this sensitive area of the IRS tax code many times and are more than equipped to assist you in your tax preparation.

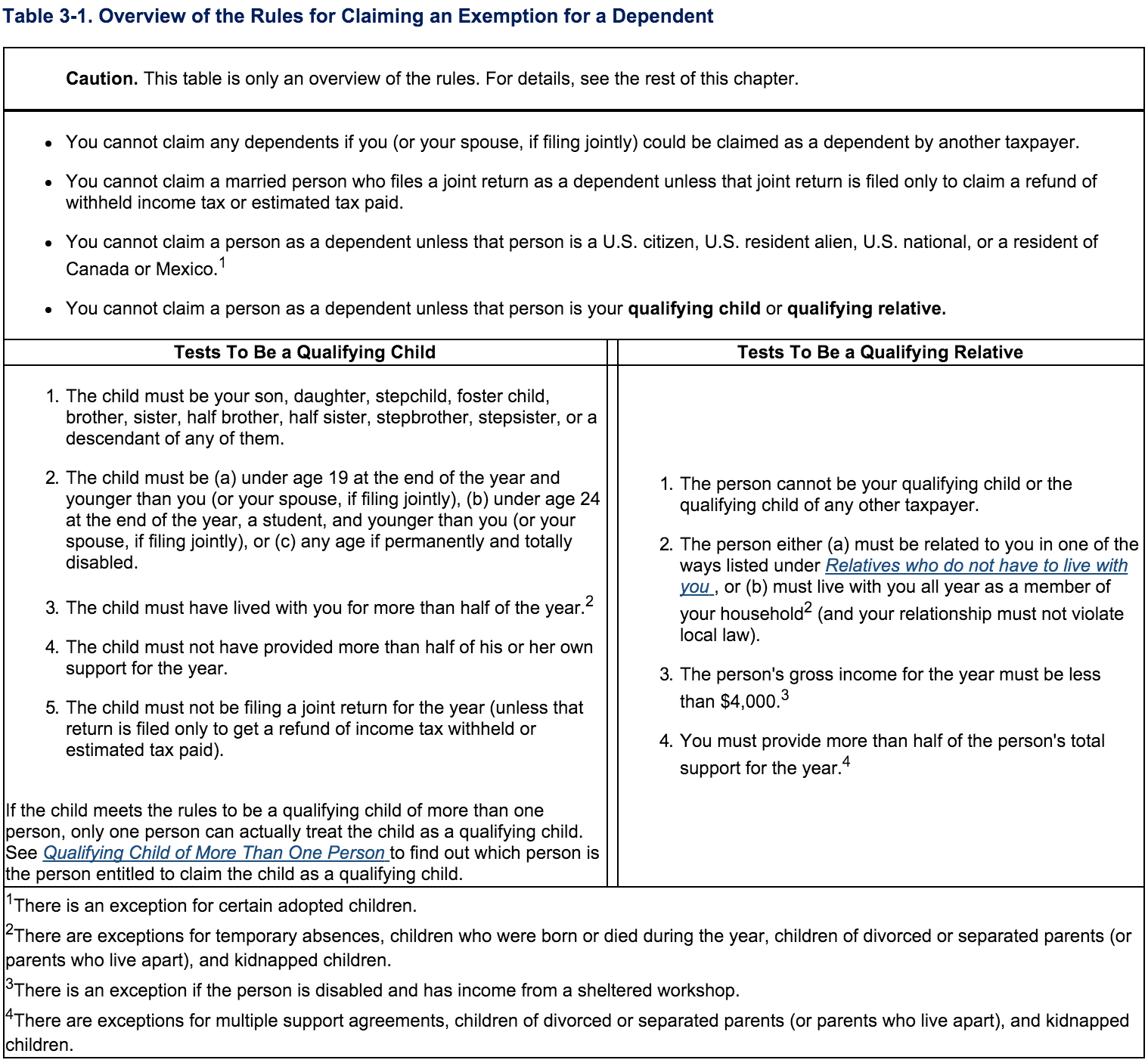

The following table taken from IRS Publication 17, Chapter 3 provides more detailed information on this tricky subject.